Check (or cheques) have long been a standard way for moving money from one bank account to another. They’re essentially little more than a codified document that puts the necessary information in a standard format to ease processing by all parties involved in a given transaction.

The check was once a routine, if tedious, way for the average person to pay for things like bills, rent, or even groceries. As their relevance continues to wane in the face of newer technology, though, the Australian government is making a plan to phase them out for good.

Put Some Respect On My Check

The pending demise of the checks was first floated in June 2023, with the release of the government’s Strategic Plan for Australia’s Payments System. With the rise of credit and debit cards, digital payments via smartphones, and Osko instant bank transfers, checks had diminished to a lower level of importance than ever.

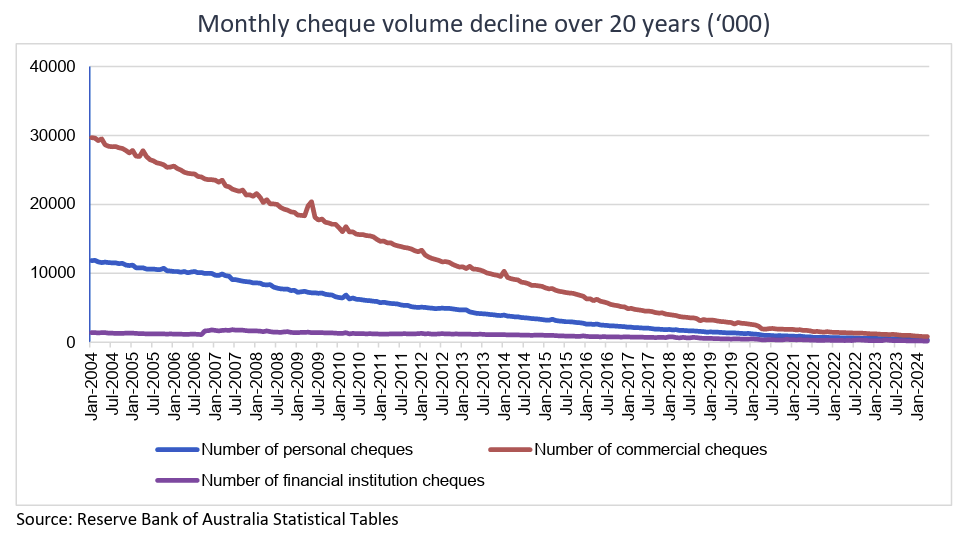

Government statistics indicated that checks were used for less than 0.1% of retail payments within Australia. In 2004, over 10,000,000 personal checks were used every month. Fast forward to 2024, and that number had dwindled to somewhere below 300,000. As volumes have fallen, the price of processing individual checks has effectively increased. In an era where digital payments happen instantly for near-zero cost, a check can take 3 to 7 days to clear, with government statistics stating processing costs for a single check now exceed $5.

Ultimately, the check is now seen as a slow and unwieldy way to make payments, and one no longer worthy of being maintained into the future. Companies have even been questioned openly in the media for the rationale of still using checks to issue refunds in this day and age. The rationale is that winding down the check system for good will lead users to prioritize cheaper, faster methods of transferring money. The aim is to reduce transaction costs, improve productivity in the financial system, and just generally grease the wheels of commerce across the country.

The current transition plan has two major milestones. By 30 June 2028, Australian banks will cease issuing personal, commercial, government, and bank checks. Any check written after this date will not be accepted and effectively deemed invalid, with no payment made. By 30 September 2029, financial institutions will cease accepting personal, commercial, government and bank cheques entirely. Any remaining checks, whenever created, will effectively be void.

These dates were chosen specifically because personal, commercial, and government checks go “stale” 15 months after they are first drawn. Thus, checks of these types that are written on the very last valid day will still be able to be cashed in the usual period of validity before the system is shut down for good. The intention is that there will be no checks that would otherwise still be valid to cash past 30 September 2029 had the system not been closed. Bank checks do not technically go “stale,” so there is still an open question as to whether there will be a need to honor unpresented bank checks after this date.

There are still a few years left until the big shut down. This gives the government and financial institutions time to ensure they have alternative payment methods in place for the handful of remaining check use cases. There are some concerns that various banks may attempt to leave the checking system prior to the government shut down date, burdening other financial institutions with the costs of keeping the system afloat until the end. The government has stated its expectations that banks will work together to ensure a smooth transition.

To that end, there are exit conditions expected to be adhered to for banks that are shutting down checking. Tier 1 banks are expected to maintain operations until the end date to support smaller institutions that rely on them for check clearing services. Additionally, banks which cease checking operations must still remain members of the Australian Paper Clearing System and fund the system. Banks will also need to provide 6 month warnings to customers ahead of any decision to shut down their checking operations.

While the domestic Australian checking system will shut down, this will not impact foreign checks coming into the country. Since these checks are processed outside the existing Australian checking system, this will not be an issue—financial institutions that process foreign checks will continue to do so.

Here in Brazil a report from our bank federation in January 2025 said that check usage is down 95.87% since 1995, and 18.4% in comparison to 2023, accounting for 0.5% of the financial operations in the country. However, even with the usage falling checks still moved little over 500 billion BRL, there’s still a lot of people here that doesn’t trust electronic payments, as well the culture of check in some places is simply too strong.

This is a little misleading; they are just eliminating paper checks, not the ACH transfers associated with checking accounts.

Here in the USA a lot of other payment methods create processing fees that someone must pay. If I want to send money to a family member and ensure they receive every dollar a check is a great method. Rental companies often charge a fee to use credit/debit since the bank does but checks are free

I’ve never seen a processing fee on debit (other than online “convenience fees,” ugh) transactions. My understanding is the typical 3% or 5% charge is because credit car payment processors are themselves allowed to charge these exhorbitant processing fees on the vendors, so they pass it along to the consumer (sometimes, or sometimes it’s included in the cost of business, so everybody effectively pays it whether they use credit or not).

This would go away if processing fees were regulated, which would on balance improve near everybody’s financial situation (except the credit payment processors), but this would also get rid of most credit card perks. Despite being better on balance, this has bad optics, which has made it very easy for lobbyists to block reform.

There are instant transfers in EU. Some opt to use them. E.g. a lot of online shops. So the payment processors bully shops into making all the checkout methods cost “0” or else. This should be illegal, for for now isn’t.

I know about the credit card processors being the source of the fee my brother runs a business and those numbers are a lot worse then 3-5% Then you see that companies like Apple create “Apple pay” aka just another fee tacked on top that did nothing.

Someone else mentioned the 0 thing and they are in general correct. If you accept Visa they will demand their users will not pay more then someone who uses cash. As such the only businesses you will see who do that are small ma pa shops who Visa don’t even know exist let alone see the sign on the counter offering the discount.

I don’t think regulation is the answer I just think we desperately need some credit card company to offer cards with lower processing fees. Although that will likely come with higher interest rates would be my guess.

“I’ve never seen a processing fee on debit”

You haven’t looked very hard, I’m afraid. Just search for “debit card processing fees” and you will be enlightened. Or appalled.

The answer is definitely not more regulation – that always favors incumbents who have phalanxes of lawyers and lobbyists. They love more regulations to raise the cost of entry. The answer is more competition. Eliminate the regulations that are stymieing competition.

this is a hilarious take, since debit processing fees used to be regulated, then recently that regulation’s implementation was challenged, leading all of that regulation to be vacated just this month. the phalanxes of lawyers are the ones leading the charge to strip consumer protections. and it’s not over yet!

“I’ve never seen a processing fee on debit (other than online “convenience fees,” ugh) transactions.”

Of course not. You never see the fees that the banks charge the retailers for credit/debit transactions. However, this fee does get passed down to the consumer. How many times have you driven past a gas station that the sign displays different prices for cash vs credit?

This whole thing is just another way for banks to separate customers from their money.

You can’t send them a simple account to account transfer? Thats a nobrainer here in europe, we dont pay for that at all. I never even seen a cheque in my life.

nope. that usually costs something like $50 a pop here.

These are free in Australia too. It’s one of the few perk of the banking cartel in .au.

have you looked at your bank fees, those checks are most certainly not free.

Ive had accounts with Chase, Capital One, Wells Fargo, Citibank, Bank Of America. The only fees Ive ever been charged for checks are the printing charges when I order new books of checks. Most major banks do not charge for cashing, depositing, or writing checks, only overdrafts, and sometimes stop payment orders.

that doesn’t mean they won’t charge fees in the future. “As volumes have fallen, the price of processing individual checks has effectively increased… Government(Australia) statistics stating processing costs for a single check now exceed $5”. Do you really think your past experience is any sort of protection against future fees? Good luck to you.

LordNothing said

“have you looked at your bank fees, those checks are most certainly not free.”

and I have. And none of the banks listed charge the fees they imply exist in any way shape or form TODAY under the terms of the accounts I have signed up for.

Sure things can change. Thats how the world works. You cant predict the future. Im just stating the facts as they are today. Enjoy Your Bliss!

I just looked at our last credit-union statement. There was a $5 fee for the entire month’s check-processing fees. I had to buy the checks, but processing them was almost free. My wife and I pay most of the bills with checks. I did walk up to the water office a mile away this afternoon though and pay the water bill with cash.

I don’t pay any fees unless I have an over draft. The bank makes money because I don’t get interest on my checking account. I keep the minimum amount in there and move the rest to the saving account and then occasionally roll that into a higher interest CD at a different bank.

With my “free” checking I can also do free bill pay. Where the bank prints a check and mails it, including paying for the postage. I use it for paying the eye doctors, the septic company, lots of things.

We still use checks for paying bills and as above for graduation present/weddings/funeral/etc. Even the credit card bill, a check is sent in. We also pay in cash at restaurants mostly. A few even have discounts if you use cash instead of credit. Checks are ‘not accepted’ in most restaurants due to stolen checks problem. That said we don’t use checks for groceries, gas, etc. That it either cash/debit/credit.

I only use cash for groceries, but other than buying gas, I only use the card when I buy online. I pay the bills (including credit-card statements) with checks.

If I pay my city electronically, including using checking account routing numbers, I get charged around $3 for a processing fee. But I can stuff a check in an envelope and buy a stamp for less than that and pay no fee.

I get hit with this multiple times. Every utility gets paid separately, so water/sewer, trash, gas (yes, it’s not part of the electric bill), electricity, property tax. All of these are monthly except the property tax and trash, so around $12-15 a month goes to some mysterious payment processing company instead of to my city government.

Weirdly I don’t get a fee for car registration if I use e-check, so at the state level they have their shit together I guess.

until last year our county assesor’s office would let you pay your property taxes on line, for a mere 5% fee; about $80 for our taxes, which are on the cheap end. And last year I had to buy more for the 1-2 I write every year (we just had some major plumbing work done, and they wanted half up front and half at the end…in checks, so at that rate we’re good for like 100 more years :-(

My city (town) has no fee for bank transfer. You can probably go in and pay in cash in person. Depends on your city. I usually give them a little more so I have no change and the extra couple dollars goes on next months bill.

Paper trail & proof of intent

A signed check is a tangible, dated record of payment. Unlike a wire or card transaction, it carries the payer’s signature and details in a way that can be legally useful in disputes.

It’s harder to deny intent when you wrote, signed, and handed over a check.

Control over timing

Writing a check lets you decide when funds leave your account — it won’t clear until deposited. With digital transfers, the money is usually gone instantly. That delay can be useful for managing cash flow.

No transaction fees (for the payer)

ACH, credit card, or wire transfers can involve fees. Checks usually don’t cost extra beyond the cost of the checkbook.

Universally understood & low tech

Not everyone has or wants online banking, especially some small businesses, landlords, or older individuals. A check requires no apps, no accounts, no smartphone — just a pen.

Security in certain cases

While check fraud exists, giving a check can be safer than carrying large amounts of cash. Unlike giving someone your bank account password, a check can be stopped with a stop payment order.

Formality & professionalism

For donations, weddings, settlements, or certain official payments, a physical check can feel more formal than “Venmo-ing” money. It often comes with a memo line for clarity.

Easier to attach conditions

Memo lines, post-dating, or “void after 90 days” can structure a payment in ways most digital platforms don’t allow.

And of course “float”.

I hate receiving checks. Instead of having money immediately in hand, now I have either go somewhere or mail it away to convert it into real dollars.

Universally understood – no, not by anyone younger than 35.

A check requires no accounts, just a pen – listen to yourself. It obviously requires a bank account.

From the receivers perspective (check cashing stores for example), not the payee. Plus even with, things like a smartphone, or the internet weren’t required for either side (some parts of the world are like this).

Most if not all banks and credit unions in the United States offer mobile (phone) deposit.

The sender has to have one, but the recipient doesn’t, at least not if he lives in any populated area with more than a few thousand people in it. “Money” stores that cash checks (for a fee) are just about everywhere that has that many people.

If you don’t have a bank account and need to send a check, send a money order instead. The recipient will treat it pretty much like a check. If you really need a check, some banks may sell you a cashier’s check, but be prepared to pay a “non-accountholder-fee” in addition to the normal “cashier’s check” fee.

If the check is drawn off a major bank you can walk into one of their branches with your ID and cash it. No account required.

It took me over an hour to do that at Bank of America. They acted like they had never heard of cashing a check.

It’s Bank of America. Normally, they’d issue you a credit card with 3x the normal rate, sign you up for some insurance that you don’t want, and slap a lien on your house for a second mortgage that you don’t have. Then, and only then, would they tell you to shove the check up your ass and take it elsewhere.

10-20 years ago an acquaintance tried to do that. The bank wouldn’t cash the check even though it was from one of their own accounts.

I’m not sure if it’s still that way today: 1) it may have been a one-off, vs. a standard banking practice, and 2) over time, major banks have gotten rid of some “bad PR” policies like this one (only to add other “bad PR” policies, sigh).

I haven’t had to go to a bank to cash a cheque in at least 10 years, probably longer. Just snap a quick picture and it’s done and dusted.

That being said, I haven’t had to do that since my company started doing direct deposit for our expenses like 5 years ago

Post dating isn’t a thing, you can write a date in the future on there if you want, but its teller discretion if it gets cashed early or not.

“Writing a check lets you decide when funds leave your account — it won’t clear until deposited.”

But does it really let you decide? You are now dependent of multiple entities, mainly, your bank, the payee and the payee’s bank. The payee might not deposit the check for a month, which can be problematic for some folks… Even of the payee deposits the check immediately, it may take a while for the banks to settle the transaction, especially if they are greedy. Your bank may withdraw the funds from your account as soon as receive the cheque, then sit on the money for a day or two before transferring it the payee’s bank, once the payee’s bank has the funds, they may hold on it for N days before crediting the payee’s account. In some cases the payee’s bank may claim (reflected on the statement/account balance) the money has been deposited, when in reality they are holding on to the money for longer.

Why are banks doing this? So they can collect interest on the money without paying it to the customer. Basically, if they are not paying you interest on a deposit, then it’s not really fully in your account. E.g a bank may claim to clear a cheque in 5 days, but interest won’t start accruing until day 10.

“Unlike giving someone your bank account password”

why would that be done?

Same as “if I want someone to send me a parcel I have to give them the keys to my house”

???

Funny that there are countries that still rely on checks. I’ve been living on this earth for more than 40 years and I can count the number of checks I had to deal with on one finger. Money is transferred from account to account across all banks in this country using the bank number and account number or, since 2016, the IBAN, which is both number concatenated with a checksum.

Over 1.4 billion unbanked so it’s a real problem.

https://www.riverty.com/en/business/insights/fintech-2040/banking-the-unbanked-will-be-the-default/

https://coinlaw.io/unbanked-population-statistics/

the big problem in the US is that bank transfers are a pull system, not a push as in europe. so you give your account number to someone and they can just take however much money they want out of your account. zero security. also they take 1-2 weeks to go through and there is no standardized method for sending electronic invoices.

What, are you joking?

No, ACH is weird. Any business knowing your account number can pull money. And these account numbers are printed on every check

I’m a supporter of digital bank transfers for lots of cases, but I can think of a number of situations where a check is really the only viable solution.

1. Class action lawsuits (I’ve gotten a few bucks from these over the years). How are they going to know my banking information?

2. Refunds from companies where you’ve paid in cash, or your credit card is no longer valid, or you’ve removed it from them.

3. Lost property refunds. I’ve had a couple of these where I was due a refund, but the company didn’t work hard to find me, so they just reported the funds as lost to the state. How will the state refund me?

4. Also, how do I send (surprise) gifts to people? Do I know my nephew’s Cash app address? More likely he doesn’t have one.

5. The “unbanked” is a huge population as well, that will also be affected here.

These are just the ones off the top of my head, I’m sure there are more.

1,3 and 5: these are problems I’ve never even heard of around here.

2: gift card or cash

4: cash

I have never sent or received coins in the mail. I have had my mail stolen. Checks work even when there are non-round numbers for someone not physically nearby. In theory, so could electronic payments, but in US practice, credit cards don’t work for paying people (or most US government-ish bills), and non-credit cards methods (like gift card good only at Amazon or the dozens of venmo/zelle etc apps) are all vendor-locked, with a side order of nearly unbounded risk for both parties. Depositing a check – even a bad one – at least won’t leave me much worse off than if I hadn’t gotten paid in the first place.

I don’t think this jives, the maximum extra it will cost you to round up to the next dollar bill is 99 cents, and checks cost you way more than that. It’s not a question of sending coins (but honestly coins should go away, I nominate the penny and the dime as first to go.)

The US penny is going away. The US Treasury announced in May that they will not be ordering any more blanks for pennies and will stop making them as soon as the blanks run out.

https://www.npr.org/2025/05/22/nx-s1-5407493/no-more-pennies-one-cent-treasury-stop-minting

Coins should not go away unless you’re okay with never paying under a dollar for anything. At current USD values, I would not be okay with paying a whole dollar for a individual banana, apple, or peach at the grocery store. Inflation still has a long way to go before those numbers make sense, and I don’t know of anyone rooting for them to get there.

Visa gift cards are such a scam; I’ve never been able to spend every last cent on one and always have a small amount left over that’s too small to be able to buy anything with (and they don’t let you withdraw cash from the card, add it to cashapp or many times even PayPal). I get offended when I’m offered a prepaid credit card instead of a check; it’s known due to either losing the cards or not being able to spend all the money a certain predictable percentage of the funds issued won’t be redeemed, which is why companies love them.

They send you a letter or email that says “Lawsuit says you get money, log in and provide account info to claim”

They send you a letter or email that says “you get refund, log in and provide account info to claim”

When you go to Lost money website they have you enter your banking info instead of an address to send a check.

You buy a gift and mail it. You click this item is a gift and put in their address. Or you call your sibling and ask “whats nephews cash app address”

The unbanked are already stuck taking checks to check cashing places and losing Up to 12% of their funds. Theyll either have to get banked, or get one of those prepaid cards that accept payments in place of bank accounts

While cheques are incredibly inconvenient, those all sound like downgrades to me.

The first ones are a security nightmare, considering financial institutions think they’re immune from looking exactly like phishing sites.

The gifting one is fine. TBH I think putting cash in an envelope is the solution.

Nobody chooses to be unbanked though, so just “get a bank account” doesn’t work. Prepaid cards suck compared to cheques because there are loads of tiny fees and you never can use exactly all of it.

In the end the only thing better than cheques in these situations is cold hard cash but nobody wants to deal with it.

The only place I’ve found recently that wouldn’t take cash was the local FedEx office. I said, “Fine, I’ll take my business elsewhere.” The only other place was probably 35 years ago when I went to a video-rental store. (Remember those?) They wanted you to have a card similar to a library card, connected to a credit card, I suppose. I told them I wouldn’t be patronizing them. I try to always have exact change, so they can’t use the argument that they don’t have the right change.

In fairness a video rental place needs to be able to hold a value equal to replacing your rental if you don’t return it. If it’s $30 per tape and you get it back it is incentive for you to honor the contract instead of walking away with their tape. They are not in the business of giving away tapes/DVD for the price of a rental.

In the US, lots of places won’t take cash. For example, hospital/health center – around here, Kaiser stopped accepting cash long time ago. Parking is another place. I see many garages and places where used to be parking meters, where you now need a credit card (and sometimes a cell phone or smart phone). Also road/bridge tolls. Many of them around here are members only affairs where not only do they not take cash, you need a special device or they charge you huge extra fees. Sports arenas.

Some government offices around here no longer accept cash.

In .au (the subject of the article) you certainly don’t have a choice. Businesses can’t pay employees in cash, they must use electronic transfer (to a bank account). To file a tax return (or receive a tax refund) you need a bank account… The kicker is that most accounts have a monthly fee. Most accounts have some kind of deal whereby if you deposit some minimum amount, the monthly fee is waived. So only poor people have to pay the fee, which makes them even poorer. Yes, in Australia, the banks charge poor people more. It sucks.

I’m 40 years old and I have never seen a check in real life. I only know that they exist from movies and TV shows. It’s such a weird concept to me. You give it, but the person might not cash it in right away. Then months later, the person caches it in and you might not have enough in your account at the time. Or you drop it, loose it, it get’s wet, and you don’t have the money anymore. It makes no sense to me to use it.

I got a debit card when I was maybe 8 years old, but wasn’t allowed to use it yet. I now have a credit card I almost never use (only used it once for an online store that didn’t have other payment options). I don’t like that you can go into debt using that card. The reason I even have a credit card is for when I travel as a backup. Only had the card for 5 years now. Been on several holidays before I had a credit card, visited several continents, bought a house, cars, etc.

I either use cash, debit card, wire transfer, online payment system through debit card or silver/gold to pay for things. I think those are enough options.

Every place is different I guess. Last I checked about 30% of my country has a credit card and even less use it and according to the news, the amount of people that have and use a credit card is declining.

“You give it, but the person might not cash it in right away. Then months later, the person caches it in and you might not have enough in your account at the time. ”

Businesses might find the delayed cashing of checks annoying for accounting reasons, but that should have no impact on the individual.

When you write a check, you update your register, subtracting the amount for which the check was written. I have NEVER had a check bounce in my life, because I don’t write checks for amounts exceeding what my register says I have in balance.

That said, I am much more concerned about efforts to eliminate cash than I am worried about the future of checking. For all the convenience of digital finance/transactions, I am deeply suspicious of it… particularly it’s potential for weaponization by the state.

What is a Register? Genuime interested question from someone aged 42 who has never used a cheque as they were abolished in The Netherlands when I was 17.

Google “Cheque Register”. Basically, it’s a ledger of check’s you’ve written so you always know your balance. Back in the days when people wrote multiple cheques in a day and didn’t have online banking, it was very helpful. It was also a tool to audit your bank statement, which was mailed to you in dead-tree form once a month. I still write cheques occasionally, but I haven’t bothered to keep a register in a very long time.

Ahh, the little stub that stays in the chequebook? I think the cheque system in the Netherlands worked differently as they were tied to your bank account, so you could always overdraw if someone else (like the energy company) withdrew from your account.

How can you POSSIBLY be 40 and yet have NEVER seen a cheque? I find that almost impossible to believe. I would not believe it except I don’t see why you would be lying over something like this. Why would you or anyone else lie about not seeing a cheque?

I remember in the 1990s having to use cheques to pay for things – like not in person things. There was no other way. Just like for earlier decades. And as someone else said – you can keep track of cheques in ways you can’t with say wire transfer. And as for those who say send cash in the post. You know how often this gets stolen? And there’s no way to track it.

Not everyone lives in the USA, where banking is about a hundred years behind the civilised world. I am 55 years and haven’t used a cheque here in Europe since the mid nineties.

In the Netherlands, debit cards were introduced in 1985 (when I was 2) and were so commonplace that the cheque system got abolished in 2001 – when I was 17.

I have seen my parents use cheques. My aunt in France still uses cheques occasionally. But I have never had the option of using them!

Debit card electronic payments were introduced in 1985. Debit cards with ATM’s are older (1979) but the debit card itself is even older – but just as a card that holds your account number.

The thing with a credit card is they take care of fraud. With a Debit card fraud your bank account can be drained or frozen.

you know grandma sent me a check for my birthday. when i got to the bank i was swarmed by no fewer than six bankers who wanted to see what it looked like to cash a paper check. they looked at me like some kind of luddite (your computers are still running cobol ffs) because i dont like becoming dependent on voodoo machines. take the check!

I understand that NZ has already phased out checks, which made it very difficult for someone I know to deposit a US tax refund.

At mt small engine shop, we accept cash or check only. Period. We do not have a way to process credit/debit cards, nor do we have any desire to. We do not own cellphones, and we don’t take electronic payments, either.

My question about all of this is why the government is able to demand that banks n longer issue or accept checks. Should that not be up to the banks and the individual retailers? If XYZ Bank WANTS to issue checks and ZZZ Retailer WANTS to accept checks, what business is it of Big Brother’s?

to answer your question, banks are generally regulated, either by law or by a banker’s association. so rules are common across all banks — otherwise, checks couldn’t work in the first place. and this sort of change is generally a negotiation between government and banks…between them, they can make the decisions without much recourse to consumers or vendors.

it’s kind of not a big deal so long as everyone follows the step of making sure there’s a good alternative in place, before getting rid of checks. you imply some “what abouts”, and the change works out so long as most of the what abouts are answered.

You can still write or accept a personal IOU. But lots of people won’t want to accept them; a check is already safer and easier to use than a personal IOU, because of what banks and the government do. They plan to stop providing that service. They might be able to do an our-bank-only version, but … That isn’t much better than a personal IOU unless you know and trust that particular bank.

The banks and businesses hate dealing with cheques, and have for a very long time now. The only reason they still do is because the government requires it. So it’s not “the government is forcing banks to stop accepting cheques”, it’s “the government is no longer forcing banks to continue accepting them.”

Not that I am disputing you, but from what source are you getting that?

I worked in the financial industry many many moons ago providing printed/mailed cheque disbursements for countless companies. It cost them a lot of money, and even then it was blatantly obvious all sides of the industry wanted it to go away asap.

Literally everything requiring paper had huge overheads, and that was back when there was actually still significant usage of the system.

At MY small engine shop we refine our own iron ore and only accept Roman coins. Since that’s older, it’s obviously better. You know the government issues that newfangled paper cash? And you trust it?

The state is able to demand these things because without a standardized and well-regulated financial system nothing interoperates and fraud (or at least arbitrage) is much easier. I think it’s pretty laughable to defend banks from “Big Brother” when large financiers and capital interests basically write the laws. You’ll be happy to hear that consumer financial protections are currently being obliterated in the U.S. I’m sure everything will get better when that part of the government shrinks, more freedom for the poor little banks!

First of all, yeah.. I made a TYPO! 😱 The HORRORS! And since I can’t edit these… 🤷♂️ deal with it.

Did I SAY that cash/check was “better”? I neglected to say that we accept barter, too, but since that isn’t government-recognized, I didn’t think it was germane to this conversation.

To answer your rhetorical question… I also never said that I TRUST cash or checks, either. Pretty sure that the citizens who trusted the government-backed cash were a little unhappy back in 1929. As for what I DO trust – I acknowledge the buying power of whatever commodity I choose to use/accept has at any given moment. That is all.

Glad you got to show off a little of your smartassedness, though, for which we are, I’m sure, supposed to admire you. Hope you feel better now.

A single bank or two deciding to issue checks would have a pretty hard time. There needs to be a clearinghouse infrastructure or anyone accepting a check would have to take it directly to the bank on which it was drawn. That’s going to get old fast.

Wow, constant reminders that I’m older than I want to be. I’m staring at my checkbook now and have to mail a payment in today.

Reasons are same as noted above by many, but for me my credit info gets stolen or compromised enough that bank issues me a new credit card every couple of years. I’ve missed (semi) annual payments (car registration, insurance premiums etc) because my card got changed and auto-pay failed.

Why are recurring payments tied to your credit card instead of your bank account?

Wow, NEVER tie payments to your bank account. They can be nearly impossible to stop. There are a lot of Gyms that don’t take Creditcards only bank account for payment for exactly this reason.

That sounds bonkers to me. Over here, you can get regular bills to automatically come up in your bank, but you still have to authorize the actual payment. Nobody, except the goverment if you get sued for nonpayment, can just send a bill and there’s nothing you can do about it.

Maybe companies are hard to stop trying, but here, outside the US, they can at least be reverted with one mouse click. And after that you just don’t allow them to debit you anymore.

The biggest problem (I’m in Aus) is that many of the bank branches have gone – and the one that remain have long queues – and without a cheque book you can’t shift significant amounts of money around.

So the only alternative is go to a branch, potentially waiting hours, so that you can pay someone…

For example, try and buy a car, or get some work done on the house, without a cheque book and see how you go.. A long trip to the bank to do electronically – and that is without the fact that the bank accept no liability if you get the transfer wrong (ie scam, or honest mistake)…

If you give me your bank details (account number and because you’re not in Europe, SWIFT and BIC), and I could send you money from my phone’s banking app. I haven’t tried recently, but for outside-eurozone, I might need to move my lazy ass to get my identifier.

If your bank account is in SEPA which is basically “Europe” (except the easternmost parts, but including the UK), I can transfer money to you from my phone using my banking app and it will be visible (but technically not always present) on your account within 5 /seconds/. Oh, and that transfer is free.

I haven’t been inside a bank in decades, and have never been in a branch of my bank because they operate online. Most people I know don’t visit banks unless for life events (mortgage, death of a family member, …)

Americans are confused because possession of a bank account number is taken as permission to initiate withdrawals from that account.

In sane parts of the world an account number is useful only for deposits and could thus be safely painted on the outside wall of one’s house.

Well, we also have ‘social (in)security’ numbers. Which millions of companies demand from you for no good reason, and they are reasonably brute-forceable as only the last 4 digits are really important, the first 5 are your birth time and place, since knowing your age is fairly easy and most people don’t move very far from where they are born. (one reason I find these ‘personality’ or ‘name’, or birth month things in social media very sketchy, scrape enough info and identity theft is easy).

So yeah, whole system is wack over here.

One wallet company even put a fake social security card in their wallet, but people used the nukber and that account got all messed up with people paying into the retirement/benefits fund.

suddenly it occurs to me that this:

with government statistics stating processing costs for a single check now exceed $5.

is probably FUD provided by the credit card companies.

I routinely write checks because I refuse to pay the convenience fee. But the other thing they do is levy unbelievably large fines for late payments to discourage checks. I once got charged a $20 late fee for a $40 bill. At that point I created a whole new account at my bank and let them EFT from it. The bank automatically transfers $40 into that account each month. Otherwise it’s empty. It does avoid giving money to Big Credit Card, but in the end I’ll probably have 20 different accounts at my bank.

But wrt retail I definitely remember the last time I wrote a check at Home Depot, they ran it through their machine and it said, “declined” I said, you can’t decline a check, it’s a check!!!” and after considerable back and forth with the manger they put it through.

“is probably FUD provided by the credit card companies.” you can decide not to believe if you want, but this is justification for Australian government to get rid of checks altogether, so, it’s a conspiracy I guess, all these institutions working very hard, trying to convince you, even though you aren’t even Australian? American banks can decide to start charging fees for checks tomorrow, get ready for more fights with managers.

Bureaucracy has trouble scaling down. If the the check clearing system costs less than a penny per check, but also has overhead of $5 million dollars per month, that starts to look like $5/check once checks are so “rare” that they are only doing 1,000,000 checks. Whether they ever get the full savings is a different question.

It’s not FUD. Take the entire cost of all the equipment, shipping costs, and employee time per year that is required to run the cheque system, and divide it by the number of cheques that actually get processed. Since there are so few cheques being processed now, the huge overheads are no longer amortized across a huge number of transactions, and the per-cheque cost ends up being huge.

Its not 1980, tellers arent pulling signature cards from filing cabinets and comparing them with the checks. $700 with shipping gets a bank a scanner that can process 60 checks per minute. $380 gets a single feed scanner that lets a teller process a single check in under 2 seconds. The average hourly wage for a bank teller in the US is around $17.48 per hour. That works out to between one and one half a cent per check in labor costs. Sorry but huge overhead is bullshit.

The better to control your money. Its not about “cost”. Banks rip us off in ecery way and they want to lower their costs. Gimme a back log of fifty toasters, 150 calandars or Im gonna keep writing checks.

They are way behind. In South Africa usage of cheques were officially terminated in Dec 2020.

https://www.gov.za/news/media-statements/south-african-reserve-bank-discontinuation-cheques-18-nov-2020

It was just to easy to fraud for one thing.

We’ve had fraudulent credit-card charges. Fortunately the CC company figured out that they were indeed fraudulent, and the CC company covered them, and we did not have to pay those charges. They do get paid though. If we confined ourselves to use only cash or check, the fraudulent charges would not have happened.

Check fraud is a problem. No checks, no check fraud 🤷🏼♂️

Phasing out checks seems like a gift to the companies that skim a couple/few percent off every transaction that’s paid by card.

There have also been major changes to the electronic payments systems to reduce or eliminate those fees, and quite a few class actions that are increasingly not going the banks’ way over them.

People forget that you also pay money to withdraw cash, and that can be a lot more expensive if you’re not careful (a $2 fee for a $20 withdrawal from a private ATM is 10%!)

In the US (at least the parts of it where I have lived) there is no fee for withdrawing cash.

Go in to bank/credit union, give them withdrawal slip (or check made out to cash), and ID (if teller is new and doesn’t recognize me), get cash.

So what happens when there is a wind storm (or blizzard/ice storm, or hurricane, major earthquake, Carrington Event, etc.)?

If power and/or communication are out for a week or month, or more, how do you get food/water/medicines/gas/etc?

How do you pay the rent, or pay somebody for repairs/cleanup?

When the cash registers and credit card readers don’t work.

When you have no cell signal (or the cell network is swamped).

You can use cash for a while, but what do you do when the cash runs out? (Most people don’t get routine cash payments.)

What happens when somebody hacks your phone, or disrupts the electronic payment system?

If nothing else, need checks in order to pay the credit card bill.

Electronic payments feels way too risky to me. A cheque is pre-printed with the right numbers. None of the chances of a typo sending money to the wrong person and no way to get it back.

I’m cleaning out my mom’s house, and discovered some one ounce gold coins. I thought, oh great I’m ready for the apocalypse. Then after about a second, but they are:

In increments of $3,500 which is kind of inconvenient.

Who’s going to believe they are real?

And, why would anyone want gold in exchange for valuable potatoes or whatever?

Only slightly less ridiculous than those transactions in movies for uncut diamonds in plastic bags that criminals hold up to the light and agree that they are worth 20 million dollars.

Still that old movie thing of a mysterious man who has 100 gold rings on a string has a certain charm. Or a bag of fake gold Rolexs.

I’ve never used a check in my life, and I was born in 1972. I got a bank card around 1988. Stopped using cash in the late 90’s. Online shopping mostly trough Paypal with a credit card. Last 7 years I’ve been using Apple Pay. It’s very convenient when travelling in Europe. Just beep the phone. My phone is also mye car key, access at work etc.

That sounds horrible when you lose your phone.

Or when the battery goes unexpectedly flat, when you drop it on a hard surface, when you misplaced it, when it fall behind the couch (you can see it, but you just can’t reach it), when you are in a horrible accident and you can’t unlock you phone with your face and fingerprint and you can’t remember the pin-code since you haven’t used it in ages, or simply when it gets stolen.

It’s not not much different from losing your keys or your wallet. With a phone I can buy a new one, log in and still have my keys and my money.

How do you buy a new one without your keys and your money?

This scares the shit out of me. If your battery is flat (or you drop/break/lose the phone etc) then you can’t eat, work, drive…. It seems like a massive single point of failure. I have a real car key, and there’s some (well-hidden) currency in the car for emergencies. Also various caches of currency in bags, cupboard etc for when the electronic systems shit themselves. This is rare, but still happens at least once a year for durations of minutes to multiple hours. If something goes wrong with my phone, it impairs my ability to make/receive phone calls. Nothing else.

I thought the entire planet had gotten rid of cheques decades ago.

I’m in Canada. I’ve written precisely five cheques in the last decade. Three of them were void cheques to provide my banking information to organizations that would only accept it that way. I also used cash for the first time in months yesterday: felt weird, and change is annoying to carry.

So yay australia!

No, Australian banks are scum. Regardless of the present storm in a teacup about cheques, they are pricks. Record profits every year, while they close branches and tack outlandish fees onto everyday accounts. https://en.wikipedia.org/wiki/Royal_Commission_into_Misconduct_in_the_Banking,_Superannuation_and_Financial_Services_Industry

That was a few years ago, zero enforcement has been applied, and their profits continue to be obscene.

I keep a hundred dollar bill in the lining of my wallet just in case but I haven’t used cash since my favorite taco truck started taking cards a couple of years ago and haven’t written a check since at least 2010.

A friend has coins sewn into his shirt tails “for pay phones” because his mom did that when he was a child. He only stopped after 9/11 when you had to go through metal detectors all the time, but it took him years before it felt like he wasn’t wearing someone else’s clothes.

This will end the “celebrities pay with checks nobody will cash” thing, although depositing checks with your smartphone ended that a few years ago.

Supposedly Picasso liked to pay for everything by check because for small amounts nobody would cash them. Andy Warhol liked to say that as he was writing a check.

Cheques are for sirs. Proles use zelle venmo apple pay.