If you’re an old-schooler, you might still go to the local bar and pay for a beer with cash. You could even try and pay with a cheque, though the pen-and-paper method has mostly fallen out of favor these days. But if you’re a little more modern, you might use a tap-to-pay feature on a credit or debit card.

In Taiwan, though, there’s another unique way to pay. The island nation has a whole ecosystem of bespoke payment cards, and you can even get one that looks like a floppy disk!

It’s Not About The Money, Money, Money

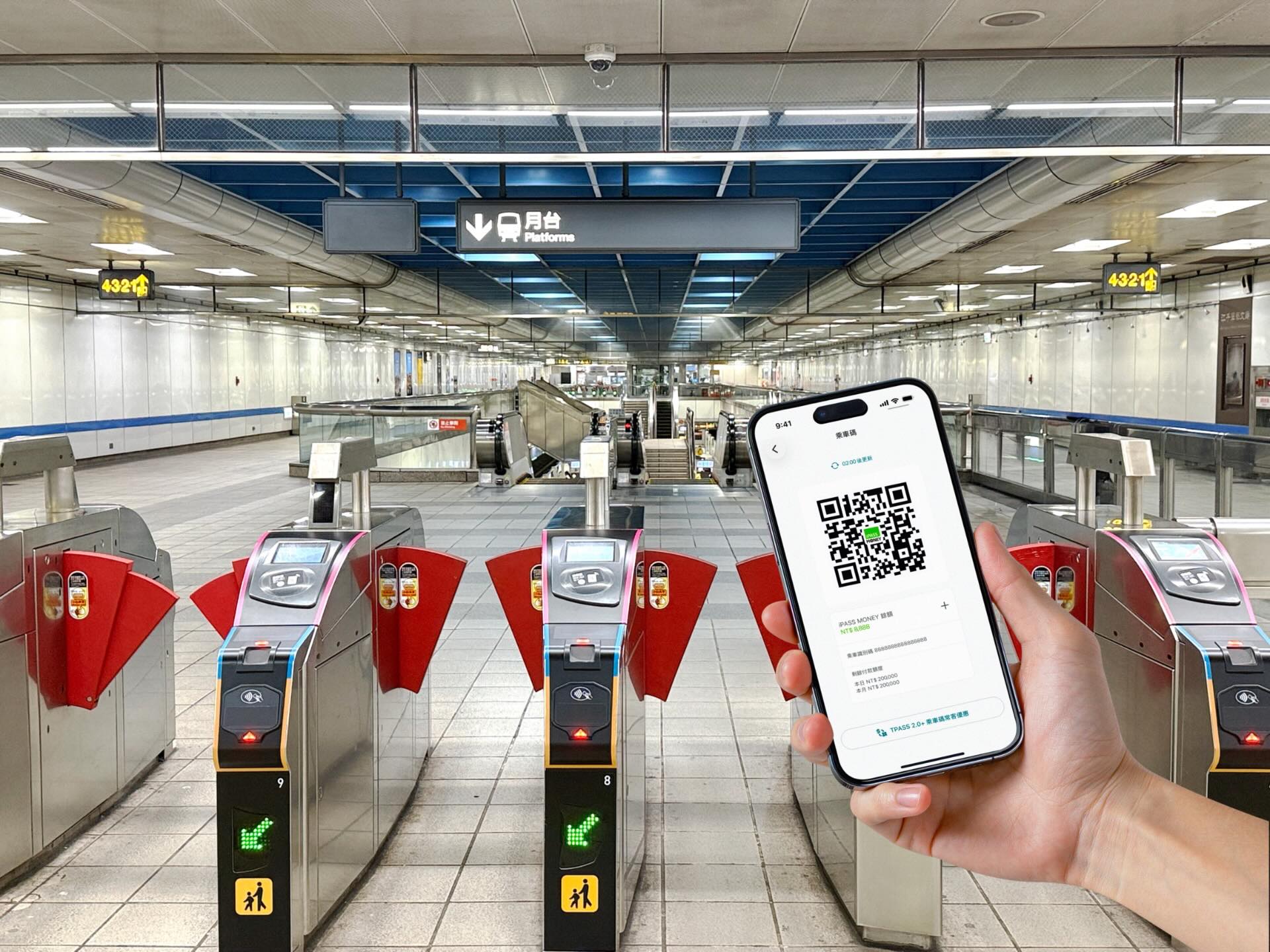

Like so many other countries with highly-developed public transport systems, Taiwan implemented a smartcard ticketing system many years ago. Back in December 2007, it launched iPASS (一卡通), initially for use by riders on the Kaohsiung Metro system which opened in March 2008. The cards were launched using MIFARE technology, as seen in a wide range of contactless smart card systems in other public transport networks around the world.

The system was only ever supposed to be used to pay fares on public transport using the pre-paid balance on the card. Come 2014, however, management of the cards was passed to the iPASS Corporation. The new organization quickly established the card’s use as a widespread form of payment at a huge variety of stores across Taiwan. The earliest adopters were OK MART, SUNFAR 3C, and a handful of malls and department stores. Soon enough, partnerships with FamilyMart and Hi-Life convenience stores followed, and the use of the card quickly spread from there.

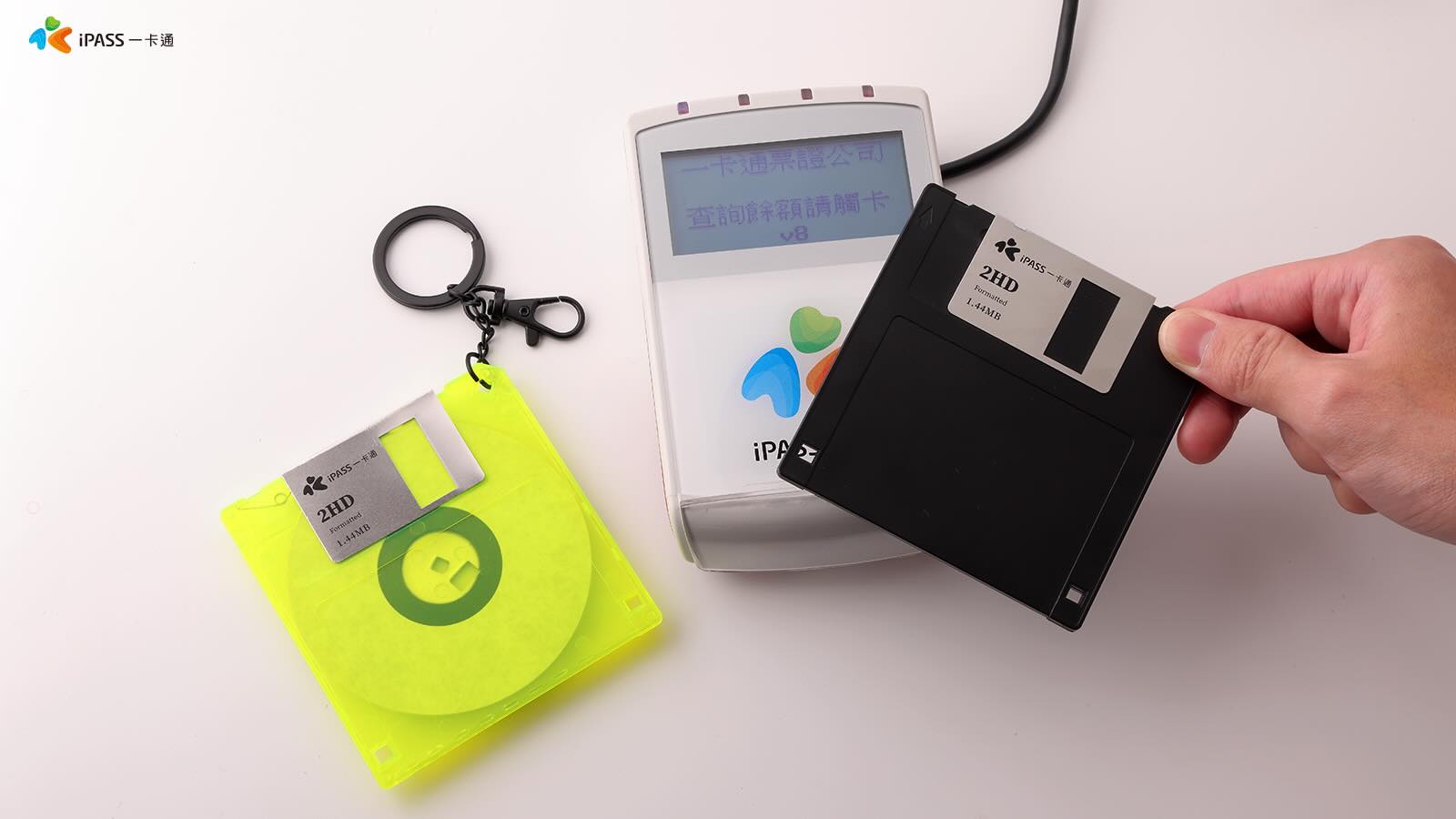

As iPASS cards continued to gain in popularity, companies started lining up to produce co-branded cards. Many came with special deals at select retailers. For example, NPC issued an iPASS card that offered cheaper prices on gasoline at affiliated gas stations. Furthermore, no longer did your iPASS have to be a rigid, rectangular plastic card. You can buy a normal one if you like, but you can also get an iPASS built into prayer beads, laced into a leather bracelet, or even baked into a faux floppy disk. The latter specifically notes that it’s not a real disk, of course; it only has iPASS functionality and will not work if you put it in a floppy drive. It is, however, a startlingly good recreation, with the proper holes cut out for write protect and density and a real metal sheath. On the translucent yellow version, you can even see what appears to be the fabric inside that would be used to protect the spinning magnetic platter.

Other novelty iPASS “cards” include a keychain-sized Taiwan Railways train and a Japanese shinkansen. Where a regular iPASS card costs NT$100 or so, a novelty version like the floppy disk or train costs more like NT$500-$600. That might sound like a lot, but in the latter case, you’re only talking about $15 USD or so. If so desired, though, you don’t need to carry a card or keychain, or floppy disk at all. It’s possible to use an iPASS with contactless smartphone and smartwatch wallets like Google Wallet and Garmin Pay.

iPASS Cards are typically sold empty with no value, and must have money transferred to the card prior to use. Notably, the money stored on the cards is backed by the Union Bank of Taiwan. This provides a certain level of peace of mind. Even if it wasn’t there, though, there isn’t so much to lose if things do go wrong—as any individual card is limited to storing a maximum of NT$10,000 (~$320 USD).

Similar Taiwanese pre-paid payment cards exist, too. EasyCard has been around since 2002, initially established by the Taipei Smart Card Corporation for use on the Taipei Metro. It similarly offers novelty versions of its cards, and these days, it can be used on most public transport in Taiwan and at a range of convenience stores. Like the iPASS, it’s limited to storing up to NT$10,000, with balances backed by the Cathay United Bank. 7-Eleven has also joined the fray with its iCash cards, which are available in some very cute novelty styles. However, where there are tens of millions of users across EasyCard and iPASS, iCash has not had the same level of market penetration.

Generally, most of us get by using payment cards linked directly to our main banking accounts. However, if you happen to find yourself in Taiwan, you might find the iPASS to be a very useful tool indeed. You can load it once with a bunch of money, and then run around on buses and trains while buying yourself snacks and beverages all over town. Plus, if you buy the floppy disk one, you’ll have an awesome souvenir to bring back with you, and you can entertain all your payment-card-obsessed friends with tales of your adventures. All in all, the banking heavyweights of the world would do well to learn from the whimsical example of the iPASS Corporation.

But it’s incredibly useful that all payment cards are the same size (wallet partitions etc)!

It would be nice if that size was about half the current size though.

I don’t know – for that day to day transport, coffee shop type spending having your bulkier but easy to find in the pocket quickly keychain style payment card is probably more useful. Certainly wouldn’t want all your cards to be that way, the real money management with all your different accounts, buyer protection offered with a credit card, the work supplied card etc you want that more regularly shaped easy to carry many of them, but when you are out and about and need to buy the train ticket or sandwich do you really want to have to read through the pile of cards to find the right one!

Tap and Pay from a cell phone.

This is that, but in a cooler form factor.

(And without the tracking, of course.)

Why? So if my phone breaks I lose all my money?

It also assumes everyone has the legal ability to use their phone as a method of payment (not everybody has that right), and that everywhere accepts your phone’s payment method (almost every business I’ve ever seen either insists on a store-specific app – so that they can be on a Legal First Name Basis with you, of course~ – or accepts Google Wallet XOR Apple Pay, it’s extremely rare to find a business that accepts both phone brands)…

I don’t put credit cards on my phone. I only carry two cards. One I use and one I use when the first one doesn’t work. I can see a crazy reusable card with no overhead that we could use like cash and it holds $100. I don’t pay with a debit card either. I don’t want people to have access to a savings account.

In China they use Wechat app for chat like Whatsapp, payments and official paperwork. Don’t go to China without Wechat. Credit cards like Visa and AMEX and cash are useless in most portion of China. For everything else is Wechat.

Sounds like a good topic for a whole article.

Never been but the idea of even a tap to pay via phone or via credit card being useless is strange to my western eyes. Please expand.

You use your phone or face for everything in China. Better bring a powerbank… oh no need you can rent them by scanning a qr code everywhere on the street. You unlock your front door with face or finger print, the lobby door with your face, scan a qr code to rent a bike, drive to the subway and scan a qr code to enter the platform. Self checkout a drink at 711 etcetc. Whole days can go by where you do not have to interact with a single human.

Good idea. In Thailand credit/debit cards were never accepted outside the higher-class establishments in larger cities. Cash was king. But over the last few years we have started using PromptPay. The vendor displays a QR code and you can pay by scanning the QR code in your banking app then entering your bank account PIN – done. It’s a bank transfer without any fees so everbody displays the QR code, even street-food sellers. I’ve used PromptPay to pay for a $1.50 meal as well as a laptop. I’ve heard of people buying a car via PromptPay. I believe it’s also possible to receive money but I haven’t tried that. The PromptPay system is usable in many ASEAN countries as well as others.

It is called UPI in India. It is very convenient. All vendors, big and small display QR code to recieve money via UPI. There is no transaction fee. Plus there is no pin required up to 2000 INR transaction (called UPI lite).

Laptops and cars? Seems extremely risky to not have a limit to the amount.

And I’ve heard about goons forcing people to pay for overcharged stuff through physical coercion in Thailand. Seems standard practice.

I see many countries solved their payments different. Recently I watched a video where a guy said about some African country where people started using pre-paid card numbers as currency for distant payments (which I dare to call a nice hack). Poland has it’s BLIK. There could be really nice article about payments.

I wonder if the card is essentially a key with the currency stored online elsewhere or if the value is somehow cryptography signed on the card itself.

I wondered this as well. A clue: You can register the card and get your money back if you lose it, or you can stay anonymous and risk losing the value.

Points to crypto on the card, and modern MiFare cards should be able to handle this.

I second all of the people above who are interested in the deeper workings of various banking/stored value card systems. We’ll see what we can do.

That is really interesting, I like that it has the option to remain anonymous in the modern world of everything turning you into the product something that just takes your money to provide a service without even wanting to know who you are as an option is refreshing.

Don’t know the underlying tech, but the Netherlands also has this option: stay anonymous or go registered.

All the discounts and money recovery are only available to registered cards.

Japan Rail’s “Suica” card fills the same role there, being accepted at many smaller stores.

I was also thinking about Suica cards, which essentially cover any merchant who might be within walking distance of a JR station. I’d heard that in the last few years, since I’ve been there last, that they’ve moved more to using phone-based payment systems, but I’ve kept my Suica card for next time.

The subway/train stations and payment for is so complicated in Japan, but kinda cool. What really helps is asking locals and they will follow you to the destination. Japan (or Asia) is weird for US travelers. I live in Alaska and even Seattle Orca card is blowing my mind.

If you got the tourism-specific “Welcome Suica” card, it expired after 28 days, losing any remaining balance.

Regular Suica cards do not have this limitation

Disclosure:- I was there in November, and used my welcome card for almost everything besides souvenirs.

Suica/Pasmo/Icoca/etc, any of the numerous cross compatible IC cards using the Sony FeLiCa chip (first used in Hong Kong, now also used in Indonesia, Philipines and even the USA) reign supreme here in Japan.

But the Paypay phone app using QR codes is hot on its heels, they seem to have tight integration with Yahoo! (Yep, that Yahoo company that died the death in the west) and Mercari.

A standard card is like cash, lose the card and you lose the value on it. However, you can get cards with your name and phone number registered to them so you can transfer any value to a new card. Commuter pass cards etc are like this too.

If you use your phone, there are ways to transfer value to a new phone too.

The Suica/Pasmo system has one annoying quirk that Android phones purchased outside Japan won’t work due to practically all manufacturers not wanting to pay the steep(!) royalties on the chip that’ll never be used, but since 2017, all Apple phones do contain the chip regardless of where you buy it due to the large adoption of iPhones in Japan and Apple’s philosophy of unified hardware.

I have also seen that Japan Rail have been putting QR code readers on the turnstiles recently, so I guess they are now accepting QR payments for those without a compatible phone or alternative payment methods (and maybe the chip shortage rattled them too after they had to make heavy restrictions on the purchase of IC cards for a long while).

It works in Asia like in Japan, but not in US. Why? Asia is like nomad people. They walk and socialize more than people in US. Personalization is more important in Asia like the Backpack Plush Animals (Labubu) that will not really work in US, because US people are car driver nation. US payment system is different in US and more solid that in Asia, but boring.

US payments system is absolutely irreversibly dominated by the few towering banks which are pretty much monopolies. Obviously, they have no interest in anything, their big bucks schema works well, yada yada yada.

Though, small fish in the pond for now are allowed to handle trifle things like small over-the-border money transfers, but there is this unspoken/unknown cap on these, too, once bank smells you are turning this into some kind of profit venture, they whack you with “adjustment fee” for doing things like Zello transfers. The limit is not known, as I’ve learned on my own, and can come out of the blue.

Regardless, US banking is now twin separated at birth copy of the UK banking, fractional reserves and blahblah, thus no longer is a competitive market place keeping tabs on unsustainable business models. It can set any condition it wants at any time it chooses, residual fees on residual fees, whatever (spoiler – I worked for a bank for 5 years, witnessed things regulators don’t care to know about, how about setting up artificially short billing period, say, 23 days instead of 30 and watch “sliding scale” slide back and forth – people caught ignoring the payment day and forced to pay late fee, aha, wonders of liberal capitalism with zero regulations).

I’ve seen ones shaped like food, little objects, even anime stuff.